Introduction

Since our last report in February, the industry is seeing distinct signs of emerging. Anecdotally we have heard from multiple operator clients around the US that March was a terrific month, in many cases exceeding preCovid #’s. This report will be the last in (let’s call it) our Covid format- where we compare current sales to what was preCovid sales. The calendar now puts us against last year’s Covid arrival. March 7, 2021 is our cutoff and we’ll end the Covid period with the six weeks ending on that date. Going forward we will refer to the “Covid Emergence Period” and soon, we hope, to “The Post Covid Period.” The way we measure will adjust accordingly.

As always, this report gives a view into the industry based on real data from a diverse set of Pinnacle client locations. We will also present an update on the status of Pinnacle’s new and future business, and share opinions of key industry operators, leaders, and groups.

I. Covid Format: Sales Performance vs Prior Year Same Period

Review of Previous Reports:

A few things to remember as you review Table 1:

- The 6-week period ending June 1, 2020 included only seven “comp” stores (open for full period both years). That steadily improved through the summer and fall.

- We got to 43 Comp stores in October before the “second wave” of Covid hit.

- Sales dropped in November through the Christmas holidays, starting to rise again in mid-January 2021, certainly including the six weeks ending 3-7-21 when our average was close to pre-Covid #’s (95%).

6 Weeks Ending 3-7-21:

Table 2 Considerations:

- The table tracks 41 Comp Stores, up from 33 in the previous report WE 1-17-21, reflecting emergence from restrictions after the second wave.

- There is a fairly steady increase in average arcade sales and percentage of previous year during the period.

- We caution that March-April sales are notoriously fickle when comparing year to year due to shifting Easter and Spring Breaks. We might take the WE 3-7-21 % of Previous Year with a grain of salt.

- 16 of the 41 stores are up over 2020 on the 6-week average, 1 is even. 14 locations are between 48-74% of last year, the balance, 10, are between 75 and 98% of 2020.

Covid Emergence Format

- For the latest six-week period through 4-18-21 we will track average sales per week for the 49 stores in this group which were open the entire period. This will be our representative store tracking group.

- These #’s are strong, the average store in the group have arcades with an annual run rate of $923k, based on performance in this six-week period.

- For perspective, sales were distributed as follows:

- Under $5k Average……………………6

- $5-10k………………………………………….13

- $10-15k…………………………………………12

- $15-20k……………………………………….. 7

- $20k+…………………………………………..11

- The consensus among operators we talked to attributed the strong performance to Covid fatigue driving pent-up demand, disposable income from Covid stimulus, and vaccination progress. This all hit during weather-transition months (still cold in many places) and during spring break and holidays.

- These strong #’s do provide comfort that our business survived and remains popular.

II. Pinnacle Business

- We completed two location installations recently one the Tonkawa Hotel & Casino Entertainment named The HUB in Tonkawa OK opening May 10. After a long Covid delay we also had a partial opening of the new entertainment center in a JW Marriott, Desert Springs, CA.

- We recently signed a multi-year agreement to represent a major entertainment and hospitality firm, The Al Hokair Group, in the US market with the mission to bring popular US concepts to the Middle East and North Africa.

- Five other projects are on Covid hold, opening dates uncertain and we have several Agreements out for signature.

III. “Taking the Pulse”- Our key takeaways from our reading and conversations with industry leaders.

Trade Shows and Webinars

- Amusement Expo has been rescheduled to June 29-July 1 2021. At this writing it is moving forward.

- F2FEC, tentatively scheduled for May has been postponed indefinitely.

- Bowl Expo: Scheduled for June 20-24, 2021 in Louisville, Ky is moving forward. We are pleased to announce that we are the featured speakers for the family entertainment session on Tuesday, June 22 from 8:30am-10am.

- We will precede our friend and client Armando Lanuti of Creative Works. Armando speaks Tuesday at 10:15am and shares how to create and maintain a corporate culture for success in the marketplace. He has certainly done that at Creative Works given the company’s consistently high-level execution while constantly innovating. Howard and I will be heading over after our session.

Congratulations Rhode Island Novelty

Congratulations to Rhode Island Novelty as it celebrates its 35th Anniversary! Let us thank them for their many contributions to the growth and development of our industry. As our client, we’ve worked with them for the last few years and witnessed first-hand the quality of the organization. Congratulations to the RINCO team!

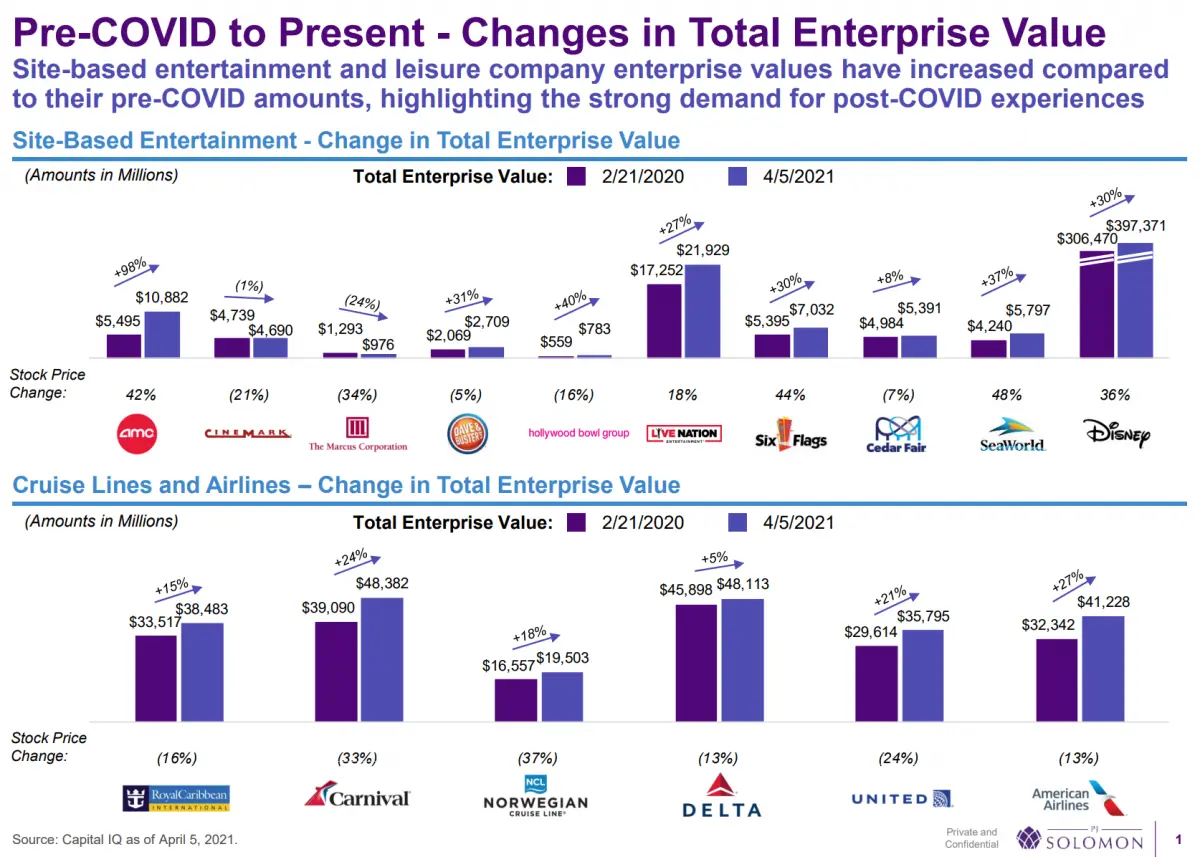

Entertainment Industry Analysis from PJ Solomon

We have grown close with the entertainment and restaurant teams at PJ Solomon, the Wall Street investment bank that is active in leisure and hospitality https://www.pjsolomon.com/. They recently issued an interesting analysis, evaluating several companies that impact our world of out-of-home entertainment centers by “Enterprise Value.”

Enterprise Value is a financial metric which may not be familiar to non-financial types. According to Investopedia “Enterprise Value (EV) is an indicator of how the market attributes value to a firm as a whole. Enterprise value [considers] the aggregate value of a company as an enterprise rather than just focusing on its current market capitalization….The market cap figure measures how much a public company is worth as determined by the stock market. It represents the total market value of all outstanding shares….Why doesn’t the market cap properly represent a firm’s value? First, it leaves a lot of important factors out, such as a company’s debt and its cash reserves. Enterprise value is basically a modification of market cap, as it incorporates debt and cash for determining a company’s valuation.”

Thanks to PJ Solomon for allowing us to share their analysis, which follows: